Mutual funds have become one of the most popular ways to build wealth in India—especially through SIPs (Systematic Investment Plans). They offer diversification, professional management, and accessibility even for small investors.

But here’s the uncomfortable truth: most investors don’t struggle because mutual funds are complicated—they struggle because of their own decisions.

Small mistakes, repeated over time, can quietly reduce your returns or even lead to losses. This article takes a deeper look at the real reasons investors go wrong and how you can avoid falling into the same traps.

Why Understanding Mistakes Matters More Than Picking “Best Funds”

Many people spend hours searching for the “top mutual fund” or “highest return fund.” But in reality, long-term success in mutual funds depends less on fund selection and more on investor behavior.

Two investors can invest in the same fund—one builds wealth, the other exits with disappointment. The difference is not the fund… it’s the approach.

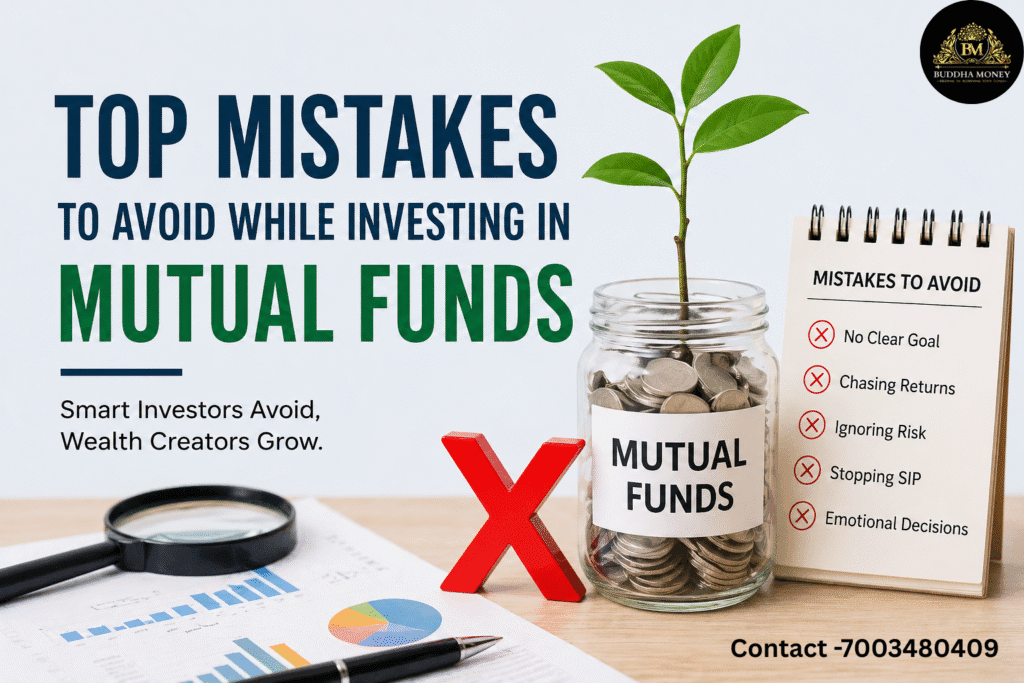

Mistake 1: Investing Without a Clear Financial Goal

This is where most journeys begin incorrectly.

A lot of investors start SIPs because they’ve heard it’s a good habit or because someone recommended it. But they don’t define why they are investing. Without a goal, there is no clarity on how much to invest, how long to stay invested, or how much risk to take.

For example, investing for a short-term goal like buying a car should not involve high-risk equity funds. On the other hand, retirement planning, which spans decades, should not rely only on low-return options.

When you don’t have a clear goal, every market movement feels confusing. A fall in the market may scare you into exiting, while a rise may tempt you to invest blindly.

What works better:

Define your purpose first. Whether it’s retirement, a house, or financial freedom—once the goal is clear, your investment decisions automatically become more structured and logical.

Mistake 2: Chasing Past Returns Instead of Consistency

It’s natural to feel attracted to funds that have delivered the highest returns recently. But this is one of the most misleading indicators in investing.

Markets move in cycles. A fund that performed exceptionally well last year may have taken higher risks or benefited from a specific sector boom. There is no guarantee that the same trend will continue.

When investors chase such funds, they often enter at the peak—right before performance slows down. This leads to disappointment and frequent switching between funds, which harms long-term returns.

What works better:

Focus on consistency instead of short-term performance. A fund that delivers stable returns over 5–7 years is far more reliable than one that tops charts for a year and disappears the next.

Mistake 3: Ignoring Your Risk Capacity

Not all investors have the same financial situation, responsibilities, or emotional tolerance for risk. Yet many people invest in aggressive funds simply because they promise higher returns.

When markets are rising, high-risk funds feel exciting. But during downturns, the same investments can drop sharply, causing panic and stress.

This mismatch between risk taken and risk tolerated often leads to premature exits—locking in losses instead of allowing recovery.

What works better:

Understand your risk profile honestly. If market volatility makes you uncomfortable, it’s better to choose balanced or moderate funds instead of aggressive ones. Investing should help you sleep peacefully, not create anxiety.

Mistake 4: Stopping SIPs During Market Downturns

This is one of the most damaging yet common mistakes.

When markets fall, fear takes over. Investors feel they are “losing money” and decide to stop SIPs to avoid further losses. But this is exactly the opposite of what should be done.

SIPs work on the principle of rupee cost averaging—you buy more units when prices are low and fewer when prices are high. By stopping SIPs during downturns, you miss the opportunity to accumulate units at cheaper prices.

Over time, this significantly reduces the overall returns.

What works better:

Stay consistent. Market corrections are not threats—they are opportunities in disguise for long-term investors.

Mistake 5: Over-Diversification (Owning Too Many Funds)

Diversification is important, but over-diversification can become counterproductive.

Many investors end up holding 8–10 mutual funds, thinking it reduces risk. In reality, most of these funds often invest in similar stocks, leading to duplication rather than true diversification.

This makes the portfolio difficult to track and reduces the impact of well-performing funds.

What works better:

Keep your portfolio simple and focused. A well-balanced mix of 3–5 funds is usually enough to achieve proper diversification without unnecessary complexity.

Mistake 6: Neglecting Regular Portfolio Review

Some investors adopt a “set and forget” approach and completely ignore their investments for years. While long-term investing is important, it does not mean ignoring performance altogether.

Funds can change strategies, underperform benchmarks, or face management changes. If you never review your portfolio, you may continue holding underperforming investments without realizing it.

What works better:

Review your portfolio at least once or twice a year. The goal is not frequent changes, but ensuring your investments are still aligned with your goals.

Mistake 7: Trying to Time the Market

Many investors wait endlessly for the “perfect time” to invest. They hold cash, expecting markets to fall, and end up missing opportunities when markets rise.

Timing the market consistently is extremely difficult—even for professionals. Delaying investments often leads to regret rather than better returns.

What works better:

Time in the market is more important than timing the market. Starting early and staying invested matters far more than finding the perfect entry point.

Mistake 8: Ignoring Costs and Expense Ratios

Expense ratio may look like a small percentage, but over long periods, it can significantly impact your returns.

Many investors ignore this factor while selecting funds, focusing only on returns. Higher costs eat into profits, especially in long-term SIPs.

What works better:

Choose funds with reasonable expense ratios while maintaining performance quality. Lower costs mean more of your money stays invested and compounds over time.

Mistake 9: Emotional Investing (Fear & Greed Cycle)

Perhaps the most powerful mistake of all is emotional decision-making.

- When markets rise, greed pushes investors to invest more at high prices

- When markets fall, fear pushes them to exit at low prices

This cycle leads to the classic mistake: buy high, sell low

What works better:

Discipline beats emotion. Having a clear plan and sticking to it helps you avoid impulsive decisions.

Mistake 10: Delaying Investments (Ignoring the Power of Time)

Many people believe they need a large amount to start investing. So they delay their journey, thinking they will begin “later.”

But in investing, time is more powerful than the amount. The earlier you start, the more you benefit from compounding—where your returns start generating returns.

Even a small SIP started early can grow significantly over time.

What works better:

Start with whatever amount you can. Consistency matters more than size.

The Bigger Picture: What Successful Investors Do Differently

If you look at investors who have built wealth through mutual funds, their strategy is surprisingly simple:

They don’t chase trends.

They don’t panic during downturns.

They don’t keep switching funds.

Instead, they focus on:

- Clear goals

- Long-term thinking

- Consistent investing

- Emotional discipline

Mutual funds are not complicated—but successful investing requires the right mindset.

The difference between an average investor and a successful one is not intelligence or access to information. It’s simply the ability to avoid common mistakes and stay consistent.

If you can control your behavior, stay patient, and follow a structured approach, mutual funds can become one of the most powerful tools for building long-term wealth.